Copper Landlocked Sequestration" Paradox: Four Policy Catalysts Determine Copper reaching $7.80 (Not Inventories)

Why record 1.1M tonne copper inventories can't prevent a 30-40% price swing—four binary policy dates (March 5, April 28, June 30, July 24) determine if $6.00/lb is a floor or a ceiling.

Executive Summary: Policy Determines Price, Not Fundamentals

COMEX copper trades $6.00/lb (February 27, 2026) amid the greatest inventory-price disconnect in 23 years. Global visible stocks exceed 1.1 million tonnes—LME 253,700t (+74.5% YTD), COMEX 538,000t (+93,000t since January 1), SHFE 290,594t (10-year high)—yet prices remain 32.46% above year-ago levels despite LME trading $44.50/t contango, signaling near-term surplus.

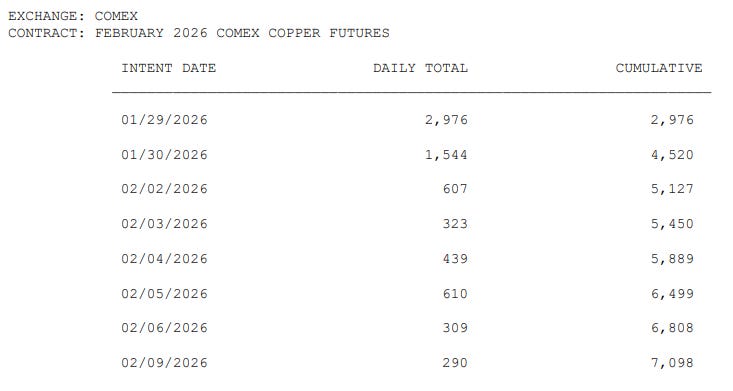

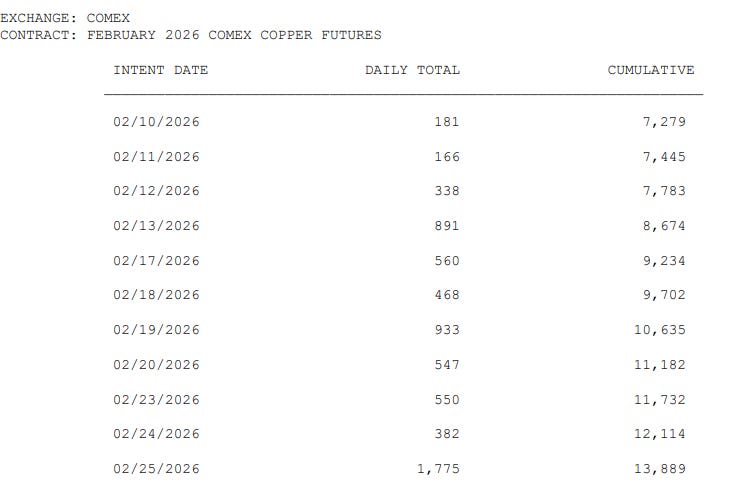

The paradox explained: February’s “record 13,889 delivery notices” (173,612 short tons) represented in-warehouse transfers, not physical extraction. Buyers took ownership but kept metal in CME-approved facilities to preserve “tariff-exempt” status for 2027. COMEX saw net inflows of +42,000 tonnes in February—accumulation, not extraction. Salt Lake City (+62,000t recent months), Tucson (+35,000t), Baltimore, and New Orleans absorbed flows as “strategic sequestration”—metal physically present but economically unavailable.

https://www.reuters.com/article/business/us-copper-stocks-sprint-to-record-high-reflecting-transport-costs-weak-deman-idUSKCN1G61JR/

Traditional supply-demand models fail because inventory location, not quantity, determines price. 538,000 tonnes of COMEX stocks are landlocked in interior warehouses lacking LME approval, preventing arbitrage to global markets. 2026 treatment charges collapsed to $0/dmt benchmark vs $21.25/dmt (2025), yet refined inventories remain elevated because 2024-2025 mine output already processed—a temporal mismatch between concentrate scarcity (Q4 2025-Q1 2026 mine disruptions) and refined surplus (prior output).